Klippa is now Doxis - Find out more

AI Document Automation ThatMakes Work More Meaningful

Reduce operational costs. Save valuable time. Prevent fraud.

Trusted by 1000+ brands worldwide

Leave Manual Document Processing Behind, Become A Frontrunner In Automation

Reduce turnaround time by 90%

Drastically reduce turnaround times by processing documents in 5 seconds, not minutes.

Maximize your workforce effiency

Empower your workforce to achieve more in less time, by automating repetitive tasks.

Save up to 80% on operational costs

Eliminate data entry work and reduce 80% of your administrative costs with automation.

Detect fraud and ensure compliance

Doxis Products

The Leader In Automated Document Processing

Empower frontline workers, reduce hiring needs, keep employees happy and innovate customer experiences. Leverage Doxis’ AI-powered document processing solutions.

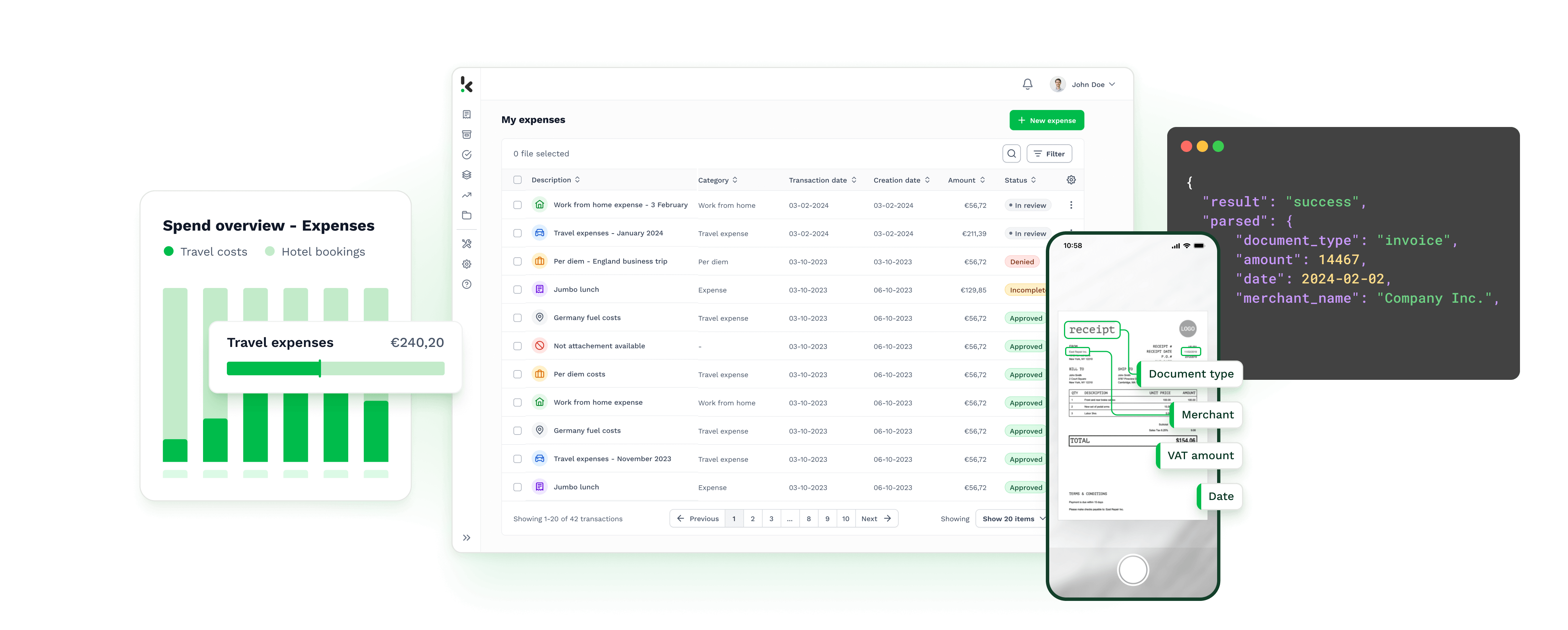

Spend Management Solution

SpendControl provides care free spend management for every financial leader. Control your organizations spend and optimize financial operations, with invoice processing, expense reimbursements and business expense cards.

Intelligent Document Processing

Doxis AI.dp helps organizations automate document workflows. Turn documents into structured data within seconds. Scan, read, sort, extract, anonymize, convert and verify documents at scale via our interface, APIs or SDK.

What Clients Say About Us

1000+ Brands Automate Workflows With Doxis

Doxis allows us to digitally register, approve, and process expenses and invoices in one user-friendly cloud environment.

We never have to worry about long processing times. The global coverage for identity documents has also been a great advantage.

Doxis’ OCR is fast, accurate, and also easy to implement. The contact with Doxis was always easy, convenient, and nice.

Maximize The Efficiency Of Your Business Processes & Teams

Our cutting-edge AI-powered document automation revolutionizes how companies digitize their data, optimize their workflows, verify document authenticity and more.

How Alasco Automated Invoice Processing In Their Real Estate Software

With Doxis’ OCR, Alasco was able to extract invoice data directly into its own real-estate software.

At Doxis, your data is treated with utmost care. We comply with global data protection and international privacy regulations.

Get Started Now!

Let Doxis’ experts show you how our smart Document Processing solutions can be integrated into your existing processes.

Discover Our Insightful Blogs

Stay informed with our insightful blogs on intelligent document processing, OCR, invoice processing, and more.