AI-powered loan processing can cut approval times from days to minutes. It eliminates manual bottlenecks and detects fraud before funding. This enables lenders to scale operations without increasing headcount while protecting profit margins.

The financial automation market is rapidly expanding, with loan volumes projected to grow significantly over the next decade. Yet, for many lenders, this growth opportunity is capped by a critical bottleneck: the manual review of loan documents.

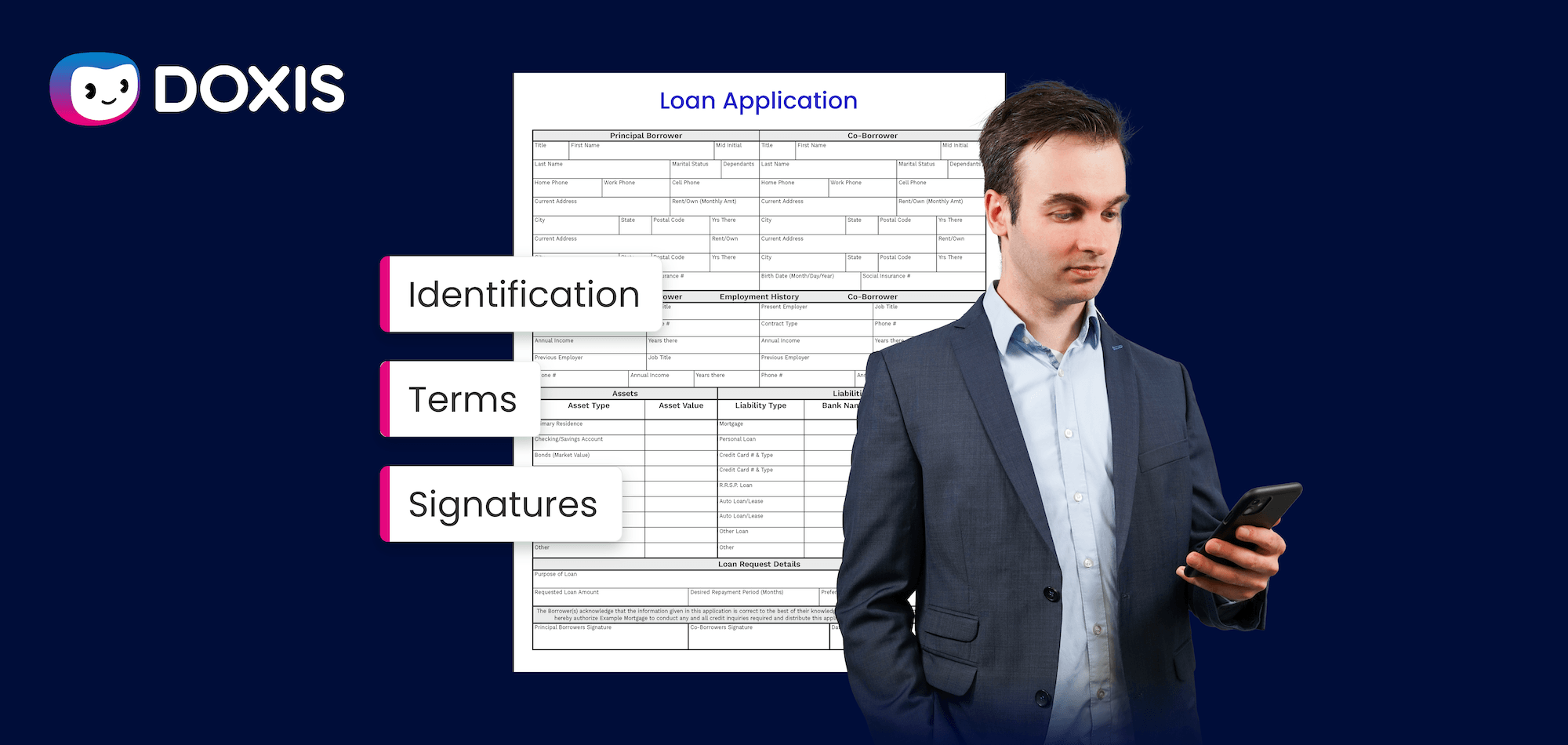

Traditionally, processing a loan application meant skilled underwriters spending hours reviewing tax returns, bank statements, and identity proofs. They had to manually enter data, cross reference figures, and scrutinize documents for signs of tampering. This approach is slow, expensive, and creates a ceiling on how much business a lender can handle without linearly increasing headcount.

Nowadays, borrowers expect decisions in minutes, not days. Automated Loan Processing changes the equation. The system handles every step of the process, from extracting, verifying data to detecting fraud. By shifting to automation, lenders can protect their profit margins, scale operations instantly, and deliver the seamless, real time experience that modern borrowers demand.

In this blog, we will explore the hidden risks of manual processing, the key capabilities of automation, and how AI can transform your lending efficiency.

Key Takeaways

- Beyond Simple Extraction: Automated loan processing manages the entire workflow including intake, verification, fraud detection, and integration, rather than just reading text.

- Scalability and Profit Margins: Automation breaks the linear link between loan volume and headcount, allowing lenders to scale operations instantly without eating into profits.

- Advanced Fraud Prevention: AI analyzes document metadata and digital footprints to detect sophisticated forgery and tampering that manual reviewers often miss.

- Speed and Customer Experience: By reducing processing time from days to minutes, lenders can offer near real time decisions, improving conversion rates and customer satisfaction.

- Seamless Integration: Solutions like Doxis integrate directly with existing Loan Origination Systems (LOS) to validate data and automate decisions without disrupting current workflows.

What is Automated Loan Processing?

Automated loan processing is the use of technology, specifically Artificial Intelligence (AI) and Intelligent Document Processing (IDP), to manage the loan origination workflow without reliance on repetitive manual tasks.

OCR in loan processing utilizes to read documents, processing goes much further than simple data extraction. It encompasses the entire journey of the data:

- Intake: Automatically collecting documents from emails, web portals, or mobile apps.

- Extraction: Converting unstructured data like PDFs of bank statements or pay slips into structured, machine readable formats.

- Verification and Fraud Detection: Instantly cross referencing data points to validate identity and checking document metadata to detect forgery or tampering.

- Integration: Pushing clean, decision ready data directly into Loan Origination Systems (LOS) or CRMs.

In a manual workflow, a loan officer acts as a data entry clerk, typing figures and visually checking for errors. In an automated workflow, the system handles the heavy lifting, allowing the underwriter to focus purely on risk assessment and decision making.

The Hidden Risks of Manual Loan Processing

Manual loan processing is a demanding task that becomes increasingly inefficient as application volumes grow. It requires staff to verify diverse documents, re-enter data into different systems, and cross reference information for accuracy. Even with experienced teams, this traditional approach creates significant business risks.

1. Document Overload and Fragmentation

A single loan application may require dozens of pages of supporting materials, each in a different format or layout. Manually sorting and interpreting this information slows down processing and creates bottlenecks. As standardized data is hard to gather from fragmented sources, decision making stalls.

2. The High Cost of Human Error

Data entry mistakes, missed fields, and duplication are inevitable in manual workflows. These errors lead to incorrect credit decisions, unnecessary rework, and frustrated customers. When regulatory compliance depends on complete and precise records, even small manual errors can be costly both financially and reputationally.

3. Vulnerability to Fraud

Fraud detection is the weak point of manual workflows. Altered documents, forged signatures, and counterfeit IDs are increasingly sophisticated and often impossible to spot with the naked eye. Without automated tools to analyze metadata and cross reference external sources, lenders are exposed to significant bad debt risk.

4. Operational Inefficiency

Manual processing binds your growth to your headcount. High operational costs make it difficult to scale profitably. Additionally, reliance on legacy systems and manual inputs makes it challenging to adapt to rapidly changing lending regulations or migrate to modern digital workflows.

These issues make it clear that traditional loan processing is no longer adequate for the speed, scalability, and accuracy expected in today’s lending market.

The Strategic Advantages of Automated Loan Processing

Manual loan processing effectively places a speed limit on your business growth. As application volumes rise, you are forced to hire more staff to keep up, which eats into profit margins. Automation breaks this cycle and offers four critical advantages.

1. Scalability Without Increasing Headcount

In a manual workflow, doubling your loan volume usually means doubling your processing team. This linear cost structure makes it difficult to scale profitably. Automated processing allows lenders to handle sudden spikes in applications without needing to hire or train new employees. You can process ten or ten thousand applications with the same core team, keeping operational costs low while revenue grows.

2. Robust Fraud Detection and Risk Mitigation

Digital documents are easier than ever to falsify. A manual reviewer might miss a subtly edited bank statement or a fake pay slip created with Photoshop. Automated processing systems dig deeper than the visual layer. They analyze metadata, EXIF data, and pixel inconsistencies to flag potential fraud that the human eye cannot see. This ensures that you are lending to legitimate borrowers and protects your portfolio from bad debt.

3. Faster Decisions and Better Conversion

Modern borrowers expect speed. If an approval takes days, they often move on to a competitor who can offer funds instantly. Automation reduces the time from application to approval from days to minutes. By providing a near real time experience, you increase customer satisfaction and improve your conversion rates.

4. Consistency and Compliance

Human underwriters can suffer from fatigue or interpret rules differently depending on the day. An automated system applies the same rigorous standards to every single application. It creates a digital audit trail for every document and decision, ensuring you remain compliant with industry regulations and internal risk policies without extra effort.

Key Capabilities of Automated Loan Processing Systems

Automated loan processing combines advanced technologies like Artificial Intelligence and Machine Learning to create a smooth workflow from application to approval. It replaces the need for manual data entry and document review with intelligent automation.

- Multi Channel Document Intake: Borrowers submit documents via email, portals, or mobile apps. An automated system collects and organizes these files instantly, identifying document types and routing them to the correct workflow without human intervention.

- Intelligent Classification and Extraction: The system uses AI to automatically distinguish between document types like passports, bank statements, and tax returns. It extracts specific fields such as names and income figures, converting unstructured files into structured data ready for analysis.

- Automated Fraud Detection: The system performs document forensics to detect tampering or forgery by analyzing metadata and pixel patterns. It also cross references extracted data with external databases and internal watchlists to flag high risk applicants immediately.

- Data Validation and Verification: The system validates information against predefined rules to ensure accuracy. For example, it checks if bank statement income matches the application. It also verifies mathematical accuracy and ensures all required fields are present and complete.

- Seamless System Integration: Automated processing solutions integrate directly with your Loan Origination System (LOS), CRM, or ERP. Validated data flows straight into your decision engine, allowing for instant credit decisions and faster fund disbursement without manual data entry.

How Doxis Enables Automated Loan Processing

Doxis AI.dp is designed to handle the complexity and variety of modern loan documentation. It serves as a complete processing layer that sits between your intake channels and your decision engine. By combining OCR, AI, and Machine Learning, Doxis transforms raw documents into verified data ready for underwriting.

With Doxis, financial institutions can:

- Process Diverse Document Portfolios: Loans require more than just an application form. Doxis handles the full spectrum of documentation including passports, ID cards, pay slips, bank statements, tax returns, and legal contracts. It automatically identifies each document type and applies the correct extraction rules.

- Detect Document Fraud Automatically: Protecting your capital means spotting bad actors early. Doxis performs advanced document forensics to detect signs of digital tampering. It analyzes metadata and pixel structures to flag forged or altered documents before they enter your risk workflow.

- Verify Identity and Data Consistency: The system ensures the borrower is who they claim to be. It cross references data points across multiple documents to validate identity. For example, it checks if the name on the ID card matches the bank statement and if the income figures align with the application details.

- Ensure Regulatory Compliance: Lending regulations are strict regarding data privacy. Doxis can automatically mask sensitive Personally Identifiable Information (PII) to ensure compliance with GDPR and other privacy standards. It creates a secure audit trail for every document processed.

- Integrate with Any System: Automation works best when data flows freely. Doxis integrates seamlessly via API or SDK with existing Loan Origination Systems, CRM platforms, and ERP tools. This ensures smooth operations without the need for extensive IT changes or system replacements.

By adopting Automated Loan Processing with Doxis, lenders are able to shorten time-to-funding significantly, detect fraud early, and deliver a faster, more reliable customer experience. This creates a competitive edge in a market where speed and precision are essential for winning and retaining clients.

To see how Doxis can help transform your loan processing workflows, contact our experts or book a free demo and explore the impact of automation on your business.

FAQ

While Optical Character Recognition (OCR) simply converts images of text into digital characters, automated loan processing manages the entire data journey. It includes intelligent classification, data verification, fraud detection, and integration with decision engines. It doesn’t just “read” the data; it validates it and prepares it for underwriting.

2. Can automated processing detect fraud better than human reviewers?

Yes. Human reviewers often miss subtle edits or high-quality forgeries. Automated systems perform document forensics by analyzing metadata, EXIF data, and pixel patterns to detect digital tampering (like Photoshop edits) that is invisible to the naked eye.

3. Does automation replace the need for human underwriters?

No, it shifts their role. Instead of spending hours acting as data entry clerks or manually verifying documents, automation handles the repetitive heavy lifting. This frees up underwriters to focus on complex risk assessments, exceptions, and final decision-making.

4. How does automation allow lenders to scale without hiring more staff?

In manual workflows, doubling loan volume usually requires doubling the staff. Automation breaks this linear link. Once the system is set up, it can handle thousands of applications as easily as it handles ten, allowing lenders to handle volume spikes without adding headcount.

5. What types of documents can Doxis’ system process?

Doxis can process a wide variety of structured and unstructured documents, including passports, ID cards, driving licences, bank statements, pay slips, tax returns, and legal contracts. It automatically identifies the document type and extracts the relevant data.

6. Is automated loan processing compatible with my existing software?

Yes. Modern solutions like Doxis are designed to integrate seamlessly with existing Loan Origination Systems (LOS), CRMs, and ERPs via API or SDK. This ensures that verified data flows directly into your current decision engine without disrupting established workflows.

7. How does automation improve compliance?

Automated systems apply the same rigorous verification standards to every application, eliminating human inconsistency. They also create a complete digital audit trail for every document processed and can automatically mask sensitive PII to ensure compliance with regulations like GDPR.

8. How much time can be saved by automating the loan process?

By removing manual data entry and visual verification, lenders can reduce the time from application to decision from several days to just minutes. This significantly shortens the “time-to-funding” and improves customer conversion rates.